Navigating the 2024 Regulatory Maze – Adapting Learnings for Outstanding Refits

2024 has long been anticipated as a year of notable regulatory change, with updates and refits across jurisdictions including* CFTC Phase 2, JFSA, EMIR (EU), EMIR (UK), MAS and ASIC. This has created a significant amount of work for clients, particularly those in scope for multiple jurisdictions. However, regulators are increasingly taking a globalized, harmonized approach, and there is no doubt that much of the work done for regulations already implemented this year (CFTC, EMIR EU, JFSA) offer useful insights for implementation for the remaining implementations (EMIR UK, ASIC, MAS).

The EMIR Refit (EU) offered some particularly relevant insights and lessons which we’ve written about in some detail in our most recent newsletter. At its simplest, it was reassuring to see that while there were some notable teething issues in week 1 (including trade repositories unable to process and send back ACK/NACK data on time, files that had worked in the UAT being rejected in production, and tracking open UTIs not being updated), many of these problems were solved for within a few days. By week 2, things were undoubtedly running more smoothly. It was also a useful reminder that the new regulations don’t just impact trading firms, but the whole infrastructure, including the TRs.

More data, in more ways, in more fields

Other challenges have taken a bit more effort. Sourcing the right data, including across the lifecycle, is one area that has taken significant amounts of effort, and will be one the market will need to keep top of mind as it prepares for EMIR UK, MAS and ASIC. Identifying and sourcing data to populate the relevant fields has taken some creativity. In the case of the trade lifecycle, this challenge can be exacerbated when it’s not clear how and when the data should be included – such as ambiguity around the requirements for reporting on cleared products where firms weren’t sure if the entire lifecycle needed to be reported, or just at give up.

Similarly, additional fields in new regulations can be problematic, and, considering the vast increase in fields for both ASIC and MAS (to 143 and 134 respectively), there’s a real opportunity for firms to proactively solve for this by looking at what was managed in the case of EMIR.

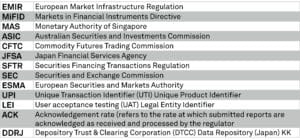

The inclusion of the unique product identifier (UPI) field has created a new data point to support and has been difficult and is likely to continue to be a source of some concern for many. Leading up to CFTC phase 2 in January 2024, populating the UPI field presented a challenge due to a lack of sufficient new UPIs ahead of go-live. By the time of the EU EMIR Refit, progress had been made but there were still a number of specific product types unavailable. The Anna Derivatives Service Bureau (DSB) is working hard to improve this, but it’s worth noting that values for some regimes are still outstanding.

Still on UPIs, a specific area that is being actively worked on is indices, with Anna DSB specifically aiming to provide more UPIs as soon as possible. On a positive note, Anna DSB provides global UPIs, with no difference across jurisdictions, facilitating firms’ ability to begin retrieving UPIs for ASIC and MAS reporting already, well in advance of go-live. This is particularly important as UPIs will be mandatory in both regulations.

Conditions and variations are not the same

Another challenge is that even as derivative reporting regulations harmonize across the globe, rules, scope, and validations vary between jurisdictions. The result is that for firms reporting across multiple jurisdictions, logic in place in one regulation may not be adaptable for other areas.

Understanding this is critical. For example, swaps are treated quite differently by ESMA and FCA under EMIR and require both legs to be reported as a single line vs ASIC, MAS, and CFTC of which FX swaps are reported as two separate legs. UTIs are also treated differently across regimes, including in the context of the use of temporary UTIs.

Even under EMIR, there are differences between the FCA and ESMA EMIR validations and rules. An example of this is how intergroup exemptions are handled/allowed. The FCA has a much higher tolerance for this than ESMA which could impact how the same trade is reported in each regime.

Leveraging Insights Across Regulatory Regimes

As financial institutions continue to navigate 2024 and the multiple changes and refits it has brought, what’s clear is that they no longer have to do it in isolation. Regulations may not be the same, and there are certainly differences that range from relatively minor ones that are easily missed to others that are intrinsic to the process firms are undertaking. But the learnings gained with each regime can be carried over, and, as importantly, increasingly, firms are able to access tools that facilitate the different data fields and data requirements.

Learn more about how Cappitech can help with your reporting, or contact us here

* Lexicon